Expect Interest Rates to Continue to Fall this Year, But This Won't Change the Abundance Of Home Sellers Set to Hit the Market

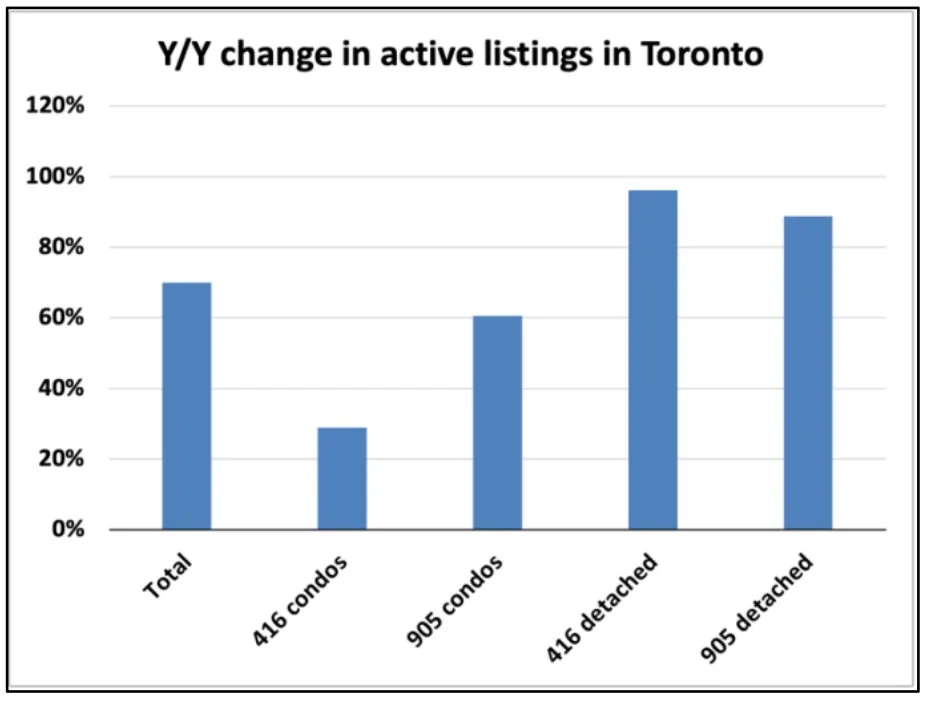

We are in the final month of Q1, and the real estate market is as murky as ever. Usually, as we approach March Break, Sellers are confidently prepping to sell their home for a heated Spring Market. January, February, and March are commonly a time of low inventory - who wants to sell their home in the cold, snowy months of Canadian winter? 2025 is breaking the mold. We saw a 49% y/y increase in New Listings in January. Sellers came out of the woodwork - and this wasn't just an increase in Condo supply.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

We are going to see New Inventory flow into the resale market this year from three main areas:

1. The completion of the biggest waves of new construction

2. Investors pulling the plug on their rentals

3. Homeowners feeling the pinch of higher interest on their renewal

The Wave of Completed Construction

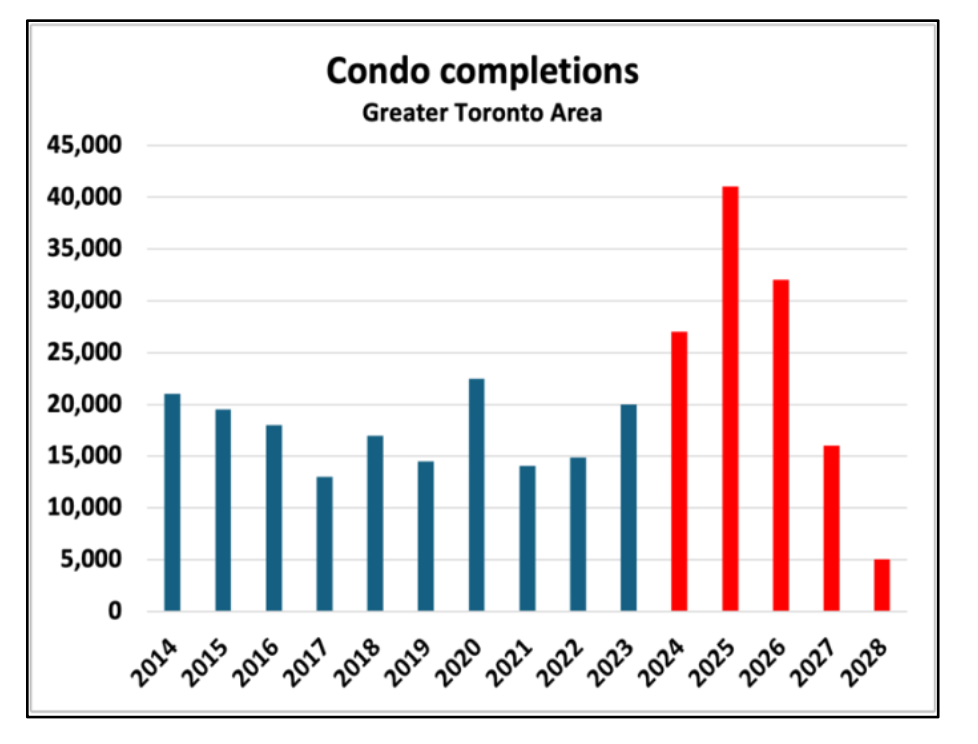

One of the major trends to watch for this year is not just what's currently on the market, but what's coming to the market. Over the last year, we saw a whopping 220,000 housing completions that added to the resale market.

Whatever it is, the way you tell your story online can make all the difference.

There's a good chance we'll see even more housing completions in 2025. We had a record number of housing starts in 2021 and 2022, with many of those being condos set to complete this year. As of Q4, we had nearly 350k dwellings in the construction pipeline in major metropolitan areas alone, barely off the all-time highs:

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

With preconstruction buyers, there is always a portion who plans to move into the property, a portion who intends to sell, and a portion who chooses to rent it. Over the past decade, most of these preconstruction buyers were investors who planned to rent their units out. However, with falling rents and high mortgage costs, we expect a polarity change, with a vast majority choosing to sell upon completion.

Investors Pulling the Plug on Their Rentals

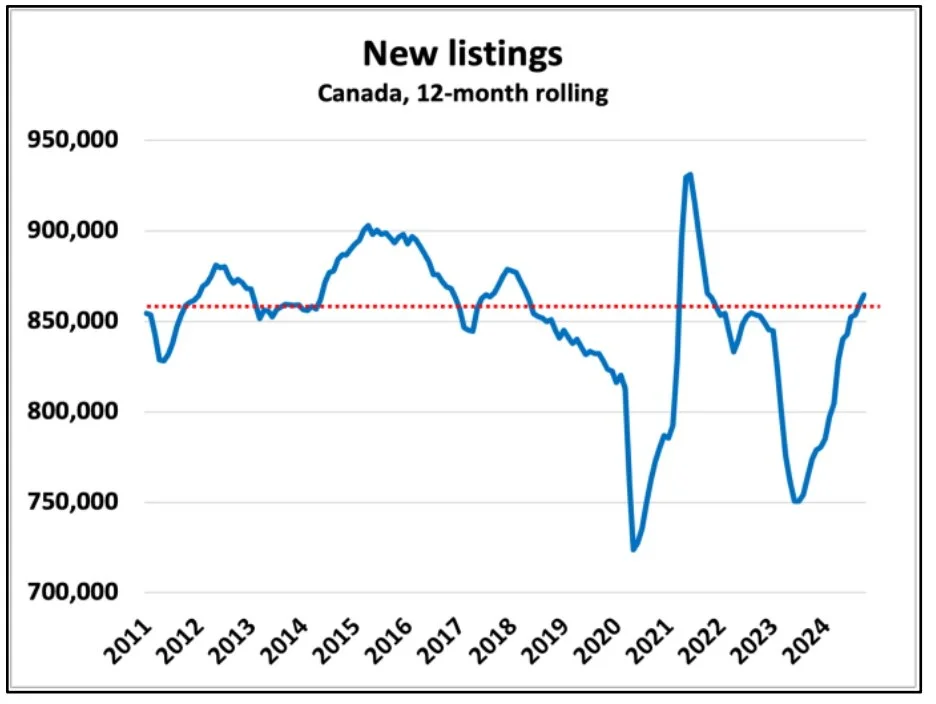

As challenging and slow as the market has been since 2022, nationally, we have seen a historically weak inflow of new listings over the past three years. We are only now back at normal levels of New Listings.

Whatever it is, the way you tell your story online can make all the difference.

The hot rental market, decline in resale prices and anticipation of lower rates contributed to this weak flow of supply. The normal flow of supply that should have come to market from typical churn in investors and regular property owners and supply from deaths/estate sales instead found its way into the red-hot rental market or sat on the sidelines. After all, no one wants to sell into a weak market if they don't have to. With the rental market cooling off, we are likely to see these properties enter the resale market.

Renewal wall expected to hit hard in 2025

Many investors already had negative cash flow on their investment property, but higher renewal rates will compound their losses. Toronto investors have been willing to bite the bullet on paying for their investments out of pocket monthly because the annual price appreciation would more than makeup for those losses. Prices have remained stagnant since 2021 (minus the 2022 peak). We expect many investors to do the math on their pending renewal and decide it's time to jump ship.

It won't only be investors who feel the payment shock. Many homeowners will face a 9% to 20% mortgage payment increase. Some of these homeowners will turn into home sellers and will try to time a sale as close to their renewal as possible to avoid steep breakage fees on the mortgage. The record number of renewals coming in '25 and '26 will likely be accompanied by ample new supply hitting the market.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

Expect Interest Rates to Continue Fall

There is some reprieve. Interest rates will likely continue to fall through 2025. Many factors lead to why we feel the Bank of Canada (BOC) will continue a steady diet of quarter-point cuts at its next few meetings. Employment in Canada is not as strong as the Labour Force Survey indicates, per capita GDP is still falling, and the threat of US tariffs - it's not a stretch to believe that the BOC may be forced to cut rates to stimulate the economy.

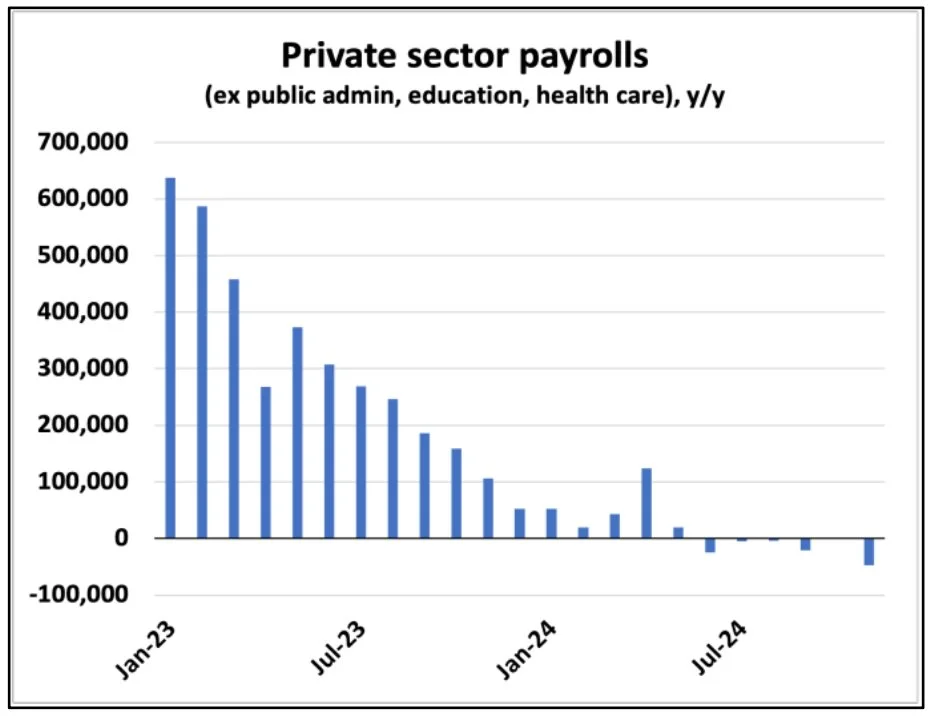

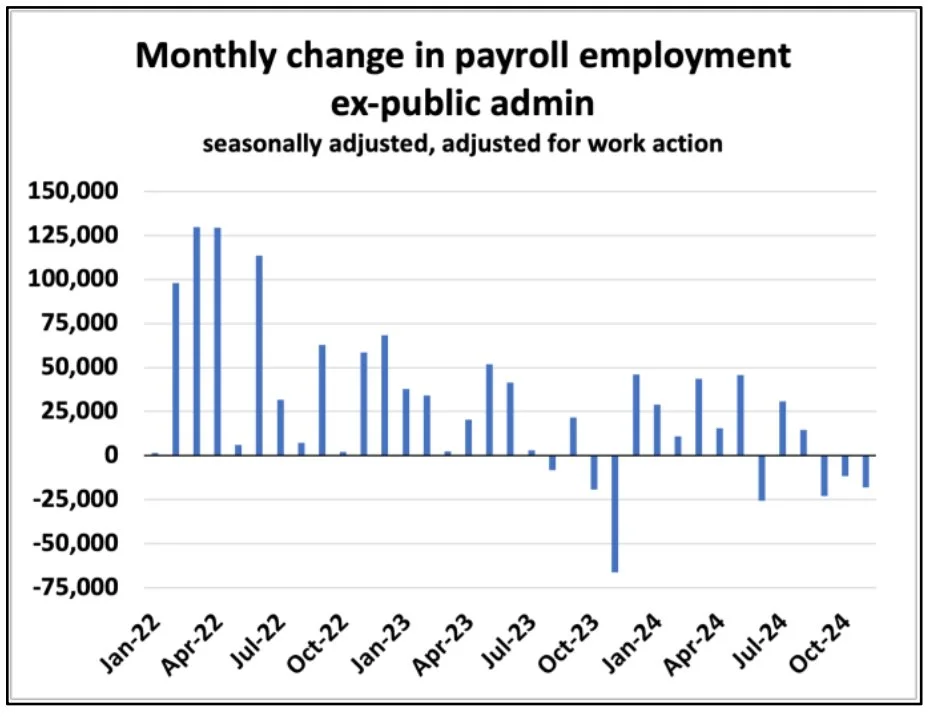

There is slack in the labour market that is not being shown in the Labour Force Survey. Canadian economist base their predictions of the market and interest rate projections on this Survey. However, the Canadian Payroll Survey is diverging. Private sector payroll is falling, job vacancies are plunging, business growth has flatlined, and unemployment is on the rise.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

Although the number of unemployed individuals is only up 20% y/y, the number of unemployed for longer than 52 weeks has doubled in the past year - something we typically see during a recession.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

An early look at the GDP for Q4 shows another per capita contraction. This marks the seventh quarter in a row of negative per capita GDP growth. Canada continues to diverge from the US in real GDP per capita; unfortunately, in the wrong direction.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

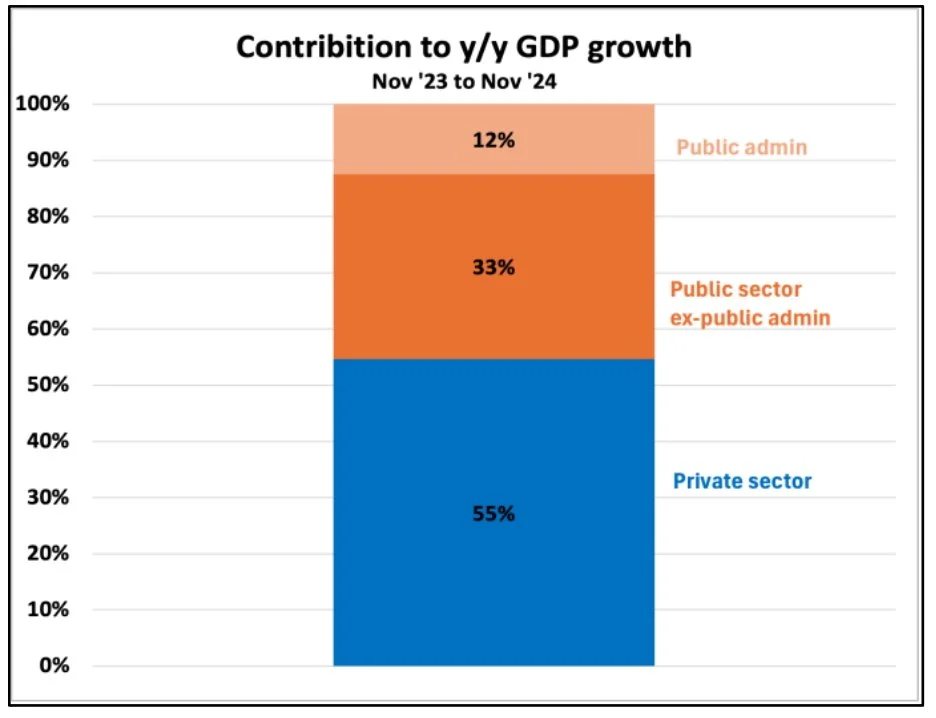

Add that 45% of GDP growth over the past year has been in the public sector, further masking the weakness of Canadian businesses at the moment.

Whatever it is, the way you tell your story online can make all the difference.

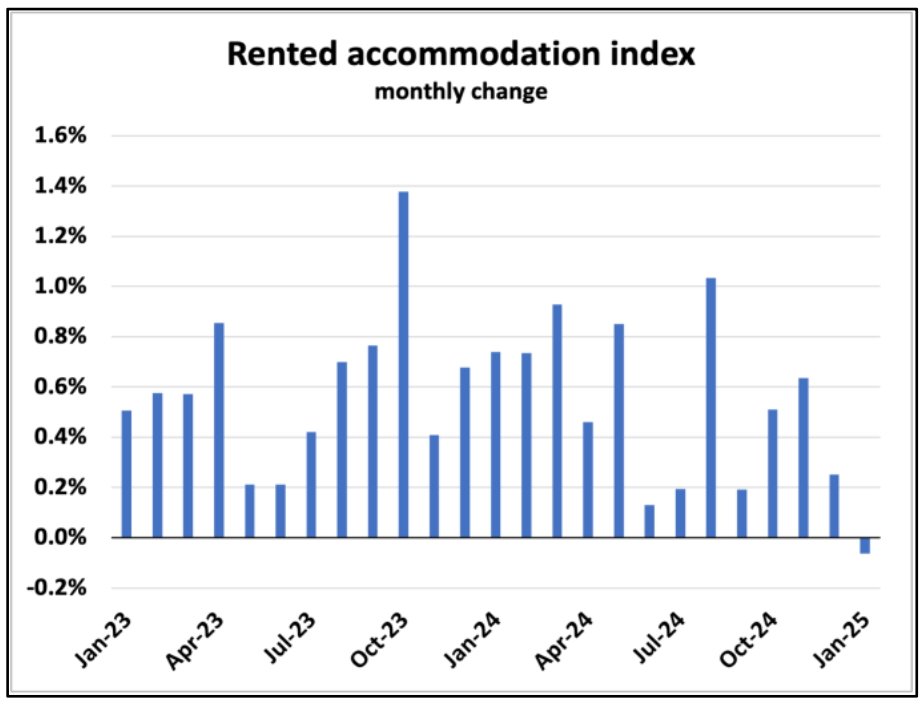

The fear of rising inflation is the largest counterargument on why the BOC will not lower interest rates. Yes, inflation will uptick, but that is a problem the BOC will contend with down the road. Headline inflation came in at 1.9% y/y for January, with 68% of the increase coming from Shelter Costs. Shelter Costs were 1.3% of the CPI, of which rents were 0.4%, and mortgage interest costs were 0.6%. Headline Inflation ex-mortgage interest costs show a flat trend since Q1 2023.

Whatever it is, the way you tell your story online can make all the difference.

Whatever it is, the way you tell your story online can make all the difference.

Many underlying threats are putting upward pressure on inflation under the surface, primarily from the weak currency and its impact on raw material costs and industrial prices. However, between falling Shelter Costs and economic concerns, the Bank will need to get rates to a level that stimulates the economy in the face of mounting signs of softness, and now the very real threats of a trade war.

For more information, stay tuned,

Cari and Paul